In order to understand the accounting information, we need to know how an accounting system captures relevant data about transactions, and then classifies, records and reports the data. One of the main components of accounting is, of course, the accounting equation.

Accounting Equation

The accounting system reflects two basic aspects of a company: what it owns and what it owes. Assets are resources a company owns or controls. Examples are cash, supplies, equipment and land, where each carries expected benefits. The claims on a company’s assets – what it owes – are separated into owner and nonowner claims. Liabilities are what a company owes its nonowners (creditors) in future payments, products, or services. Equity (also called owner’s equity or capital) refers to the claims of its owner(s). Together, the relation of assets, liabilities and equity is reflected in the following accounting equation:

Assets = Liabilities + Equity

Liabilities are usually shown before equity in this equation because creditors’ claims must be paid before the claims of owners. (The terms in this equation can be rearranged; for example, Asset – Liabilities = Equity.) The accounting equation applies to all transactions and events, to all companies and forms of organizations, and to all points in time.

Many companies maintain corporate websites that include accounting data – see Nestlé’s website (www.nestle.com) as an example. Another way is via the website of the stock exchange where the company is listed. Nestlé is listed in Switzerland so the website of the Swiss Stock Exchange (www.six-swiss-exchange.com) also provides the links to access the company’s accounting data.

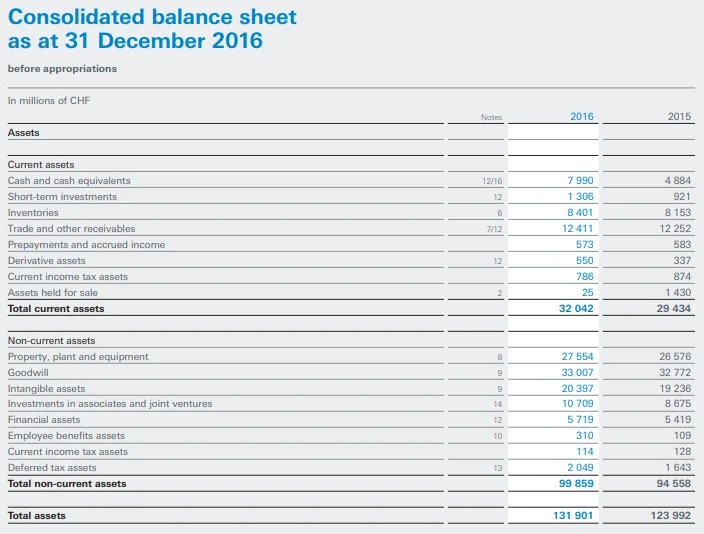

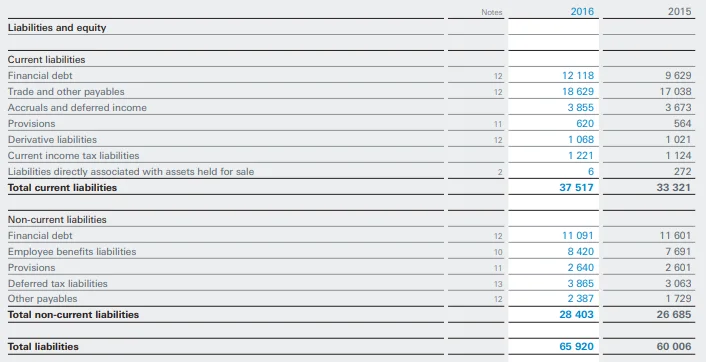

Now, let’s take Nestlé as an example. In 2016, Nestlé’s assets equal CHF131.9, its liabilities equal CHF65.92, and its equity equals CHF65.98 (all in CHF billions). – Source

Assets

Assets are resources a company owns or controls. These resources are expected to yield future benefits. Examples are Web servers for an online services company, musical instruments for a rock band, and land for a vegetable farmer. The term receivable is used to refer to an asset that promises a future inflow of resources. A company that provides a service or product on credit is said to have an account receivable from that customer.

Liabilities

Liabilities are creditors’ claims on assets. These claims reflect company obligations to provide assets, products or services to others. The term payable refers to a liability that promises a future outflow of resources. Examples are wages payable to workers, accounts payable to suppliers, notes payable to banks, and taxes payable to the government.

Equity

Equity is the owner’s claim on assets. Equity is equal to assets minus liabilities. This is the reason equity is also called net assets or residual equity.

Equity for a noncorporate entity – commonly called owner’s equity – increases and decreases as follows: owner investments and revenues increase equity, whereas owner withdrawals and expenses decrease equity. Owner investments are assets on owner puts into the company and are included under the generic account Owner, Capital. Revenues are sales of products or services to customers. Revenues increase equity (via net income*) and result from a company’s earnings activities. Examples are consulting services provided, sales of products, facilities rented to others and commissions from services. Owner withdrawals are assets an owner takes from the company for personal use. Expenses are the costs necessary to earn revenues. Expenses decrease equity. Examples are costs of employee time, use of supplies, and advertising, utilities, and insurance services from others. In sum, equity is the accumulated revenues and owner investments less the accumulated expenses and withdrawals since the company began. This breakdown of equity yields the following expanded accounting equation.

Assets = Liabilities + Equity (Owner, Capital – Owner, Withdrawals + Revenues – Expenses)

*Net income (also called net profit) occurs when revenues exceed expenses. Net income increase equity. A net loss occurs when expenses exceed revenues, which decreases equity.